life below the line...

Down Here on the Ground, Dekalb, Georgia

By Dave J. | Posted Monday December 19, 2011

My wife was ill. I had worked for over 3 years moving from company to company. When it became time to pick up the tab for insurance, it was time for me to move on to the next job. I always worked and they kept me on until the very last minute.

One day, after recovering from pneumonia, my we back to work, my wife became ill with the same respiratory illness and we could not afford to see a doctor. My wife was opposed to going to the hospital and spending the night in the ER.

She decided to wait until the following Monday when I would have enough money to pay the doctor bill.

On the night before we were going to the doctor, she suffered some kind of rupture due to excessive coughing and died in her sleep. My wife was 50 years old. He birthday was 28 days earlier.

Shortly after that, I was struck by a car and only by the grace of God was I able to survive the next 6 years. But now, I am going down slow. Every month, I have less and less and I am falling farther and farther behind. I pray that things will improve, but my horizon seems to have a picture of my losing my home, and then slowly starving to death.

Hopefully, something will happen and save me from this fate. But, I see it happening to people all around me. I wish I could say I know things will be ok, but I just don’t know any more.

I really just don’t know.

Wasted Skills, Simple Needs, Walla Walla, Washington

By Sara Ybarra L. | Posted Wednesday May 16, 2012

My husband, my daughter, my son, and myself lived on a little more than $50,000 annually for quite awhile. Many would find that hard to believe and wonder why we would do such a thing. We lived modestly in a simple house that we owned near a small town. My husband and I are college educated, but the town, which we loved, offered limited employment and mostly smallish salaries. So we were decidedly frugal, used the state-sponsored health insurance, which was generous then, and my kids were consistently on the free and reduced school lunch program. Our cars were 20 years old, back-to-school clothes were from thrift and consignment stores, Christmas from sale items, and so on. It was nothing to complain about.

Over time though, we felt squeezed. The state health insurance started raising our premiums, co-pays, and even pestering us to leave the program entirely, which we finally did do. I lost my job in 2007 and, after the shock, decided to go back to grad school (“making lemonade from lemons”). What jobs I could get were temporary, for example: for a toy catalog during Christmas, for the U.S. Census, and I even got a couple of art commissions—my husband and I are sculptors with day jobs. Then my husband’s day job with a production cabinet shop and dependent on the housing market, cut back more and more, until it was nothing at all. We hung on and kept trying to find employment, to sell our sculpture, and even built a rental unit on our property—all with credit cards and dwindling savings, which—you can imagine—was not much to begin with. And I graduated, with a shocking student loan debt.

Last December, my husband, aged 64, finally got the job he deserves, sort of. His skills are appreciated, the conditions are fair, and there are standard paid vacations, and some health insurance for both of us. But his pay is less than what he earned at his last job, and it is a full 8-hour drive from our house and town on the coast. So we rented out our house, became renters ourselves in this new town, and I am still a job hunter. Between our credit cards, my student loans, and the rent here—quite a bit more than our mortgage back home—I feel that even with our modest expectations, our depleted retirement savings, and our old cars—we’ll never recover.

What I was hoping for, when President Obama took office, was to recover our affordable health insurance and to enjoy a sort of New Deal Federal Arts Program—which once helped the arts to flourish and artists to survive the Great Depression of the 1930s. With such a program, my husband and I could have offered our best work and our most valuable talents to make sculpture for public art. We wouldn’t have needed more than a fair price two or three times a year and we would have paid our fair share of taxes unlike the greedy corporations and banks who, with the help of their heartless politicians, caused and continue to contribute to these unjust conditions. It isn’t right. We have so much to offer and ask for only a fair shake in return.

By Dave J. | Posted Monday December 19, 2011

My wife was ill. I had worked for over 3 years moving from company to company. When it became time to pick up the tab for insurance, it was time for me to move on to the next job. I always worked and they kept me on until the very last minute.

One day, after recovering from pneumonia, my we back to work, my wife became ill with the same respiratory illness and we could not afford to see a doctor. My wife was opposed to going to the hospital and spending the night in the ER.

She decided to wait until the following Monday when I would have enough money to pay the doctor bill.

On the night before we were going to the doctor, she suffered some kind of rupture due to excessive coughing and died in her sleep. My wife was 50 years old. He birthday was 28 days earlier.

Shortly after that, I was struck by a car and only by the grace of God was I able to survive the next 6 years. But now, I am going down slow. Every month, I have less and less and I am falling farther and farther behind. I pray that things will improve, but my horizon seems to have a picture of my losing my home, and then slowly starving to death.

Hopefully, something will happen and save me from this fate. But, I see it happening to people all around me. I wish I could say I know things will be ok, but I just don’t know any more.

I really just don’t know.

Wasted Skills, Simple Needs, Walla Walla, Washington

By Sara Ybarra L. | Posted Wednesday May 16, 2012

My husband, my daughter, my son, and myself lived on a little more than $50,000 annually for quite awhile. Many would find that hard to believe and wonder why we would do such a thing. We lived modestly in a simple house that we owned near a small town. My husband and I are college educated, but the town, which we loved, offered limited employment and mostly smallish salaries. So we were decidedly frugal, used the state-sponsored health insurance, which was generous then, and my kids were consistently on the free and reduced school lunch program. Our cars were 20 years old, back-to-school clothes were from thrift and consignment stores, Christmas from sale items, and so on. It was nothing to complain about.

Over time though, we felt squeezed. The state health insurance started raising our premiums, co-pays, and even pestering us to leave the program entirely, which we finally did do. I lost my job in 2007 and, after the shock, decided to go back to grad school (“making lemonade from lemons”). What jobs I could get were temporary, for example: for a toy catalog during Christmas, for the U.S. Census, and I even got a couple of art commissions—my husband and I are sculptors with day jobs. Then my husband’s day job with a production cabinet shop and dependent on the housing market, cut back more and more, until it was nothing at all. We hung on and kept trying to find employment, to sell our sculpture, and even built a rental unit on our property—all with credit cards and dwindling savings, which—you can imagine—was not much to begin with. And I graduated, with a shocking student loan debt.

Last December, my husband, aged 64, finally got the job he deserves, sort of. His skills are appreciated, the conditions are fair, and there are standard paid vacations, and some health insurance for both of us. But his pay is less than what he earned at his last job, and it is a full 8-hour drive from our house and town on the coast. So we rented out our house, became renters ourselves in this new town, and I am still a job hunter. Between our credit cards, my student loans, and the rent here—quite a bit more than our mortgage back home—I feel that even with our modest expectations, our depleted retirement savings, and our old cars—we’ll never recover.

What I was hoping for, when President Obama took office, was to recover our affordable health insurance and to enjoy a sort of New Deal Federal Arts Program—which once helped the arts to flourish and artists to survive the Great Depression of the 1930s. With such a program, my husband and I could have offered our best work and our most valuable talents to make sculpture for public art. We wouldn’t have needed more than a fair price two or three times a year and we would have paid our fair share of taxes unlike the greedy corporations and banks who, with the help of their heartless politicians, caused and continue to contribute to these unjust conditions. It isn’t right. We have so much to offer and ask for only a fair shake in return.

life as the 1%

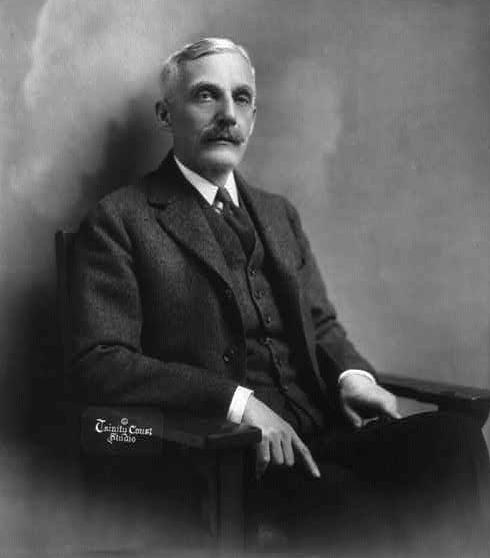

Andrew W. Mellon

Peak wealth: $188.8 billion. Age at peak wealth: 80

Andrew William Mellon was the son of a Pittsburgh banker Thomas Mellon (who founded the Mellon Bank). Andrew got his start early: he started a lumber company at the age of 17 and by the age of 27 had taken over his father's bank. He also got into oil, steel, shipbuilding, and construction business.

In 1921, President Warren G. Harding appointed the financier Mellon as the Secretary of the Treasury, where he served for 10 years (under three U.S. Presidents). At that post, Mellon increased federal revenue by decreasing the taxation rate and cutting federal spending.

Peak wealth: $188.8 billion. Age at peak wealth: 80

Andrew William Mellon was the son of a Pittsburgh banker Thomas Mellon (who founded the Mellon Bank). Andrew got his start early: he started a lumber company at the age of 17 and by the age of 27 had taken over his father's bank. He also got into oil, steel, shipbuilding, and construction business.

In 1921, President Warren G. Harding appointed the financier Mellon as the Secretary of the Treasury, where he served for 10 years (under three U.S. Presidents). At that post, Mellon increased federal revenue by decreasing the taxation rate and cutting federal spending.

comparison

Obviously there is a clear and distinguishable difference between the wealthy and the poor. However, in these specific stories, the poor and the wealthy are both hard working yet end up with very different results. This is seen throughout today's society; people working multiple jobs trying to support a family and just not making ends meet. However, it seems to be becoming more rare to see wealthy people working hard. A lot of today's rich people were blessed with something wonderful called inheritance. meaning they really don't need to work at all, therefore they don't. Not to say that all poor people work hard...but people such as the ones in these stories do, and they deserve a hand up.